The New Insurance Environment

Insurers and brokers who anticipate and plan for change can shape their own future, writes Ramzi Ghurani.

What a difference a year can make. The COVID-19 pandemic and the resulting economic fallout have radically shifted personal and professional needs, expectations, and habits. In the wake and disruptions caused by the pandemic, the insurance industry stands on the precipice of profound change. Furthermore, we witnessed the virtualisation of organisations and insurer operations without warning.

Whether it’s increased digitisation, meeting the growing demands of consumers, or the introduction of new competitors, there are many obstacles we will encounter as we look towards the new insurance environment. However, one thing remains certain: the insurance sector is ready to rise to the challenges that lie ahead.

What’s Changed Over the Past Year?

Shift to remote working

Internally, the insurance industry witnessed historic changes as well. For example, in areas hit hardest early in the pandemic, upwards of 90 percent of operations shifted without warning to a remote workforce presence. While there were some initial bumps in the road, most insurers adapted to the new virtual environment, leveraging existing and emerging technology.

This rapid shift did not present without unique challenges. A newly deployed remote work staff required clear and effective communication between leadership and staff to ensure all expectations and processes were in place and functioning smoothly. Additionally, communication was needed between staff and insurance clients to understand any/all issues impacting performance and to gauge progress against deliverables.

Channel overload

Right out of the gate, insurers around the world faced a huge spike in consumer demand. Whether it’s about travel insurance, critical illness, business interruption, or something else, customers are inundating insurers. Concerns included what was currently included in their coverage, what coverage they would like moving into the future, as well as filing claims against their current policies. This challenge led many companies to reevaluate internal resources, adjust their specialist teams, and create more agile ways of working to meet the rapidly evolving demands of their clients.

Digitisation

From late 2019 to recent months, insurers around the world found those with more advanced digital underwriting, claims and administrative processes in a much stronger position than others. Insurers without these capabilities or those who rely on cruder technology workflows are more likely to struggle as we move into the future.

Increased risk of fraud

Unfortunately, during times of crisis there are those who seek to exploit through fraudulent claims. Fraud is not limited to insurance claims themselves, but also though remote working. Unless a company has the right control measures in place, remote workers could run the risk of hacking attempts by bad actors seeking to take advantage of vulnerabilities to obtain customer data, siphon off financial information, or disrupt services. It is essential for cyber and forensic teams to work directly with IT teams as stresses on the system increase, recognising any potential risks for a security breach.

What Challenges Will Drive the Future of Insurance?

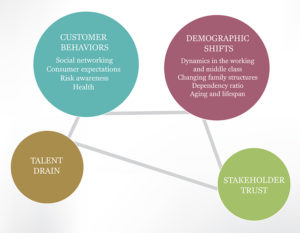

Social: The balance of power is shifting from the insurer towards the customers. Moving into the future, progressive insurers will need to adapt to the needs of self-informed consumers looking to protect their interests and cash flow.

- Customer Behaviors

- Social networking

- Consumer expectations

- Risk awareness

- Health

- Demographic Shifts

- Dynamics in the working and middle class

- Changing family structures

- Dependency ratio

- Aging and lifespan

- Talent drain

- Stakeholder trust

Economic: The rise of political and economic power in emerging markets work to create truly global markets with products that are able to seamlessly integrate regardless of location

- New opportunities

- Fiscal pressure

- Business interruption

- Inflation/deflation

- Urbanisation

Technology: Innovations in hardware and software, coupled with increased digitalisation, will transform data into tangible and actionable solutions.

- Analysis and information

- Software and applications

- Increased remote workforce

- Protection against cyber threats

Environmental: With catastrophic events on the rise and lack of data to predict them, insurers will need to adapt and create innovative solutions. To meet environmental challenges, insurers will need to look towards the rise of more sophisticated risk models and transfers to address the increasing severity and frequency of catastrophic events.

- Climate change and catastrophic events

- Pollution

- Sustainability

Political: Standardisation and globalisation of the insurance market will continue to challenge insurers to navigate local, regional, and global regulations across insurance products and practices.

- Regulatory reform

- Geopolitical risk

- Terrorism

- Tax regulations

- Takaful Compliance

Although the future is hard to predict, it’s not impossible to prepare for it. While insurers are grappling with the fallout of the global pandemic, those who anticipate and plan for change can shape their future. Those who do not anticipate these changes will need to remain agile enough to follow the lead of industry leaders.

MENA insurance sector

Ramzi Ghurani, managing partner, Petra Insurance Brokers

As with organisations across all global sectors, those in the Middle East and North Africa (MENA) region are feeling the impact of transitioning insurance markets. Aside from the obvious fallout associated with the economic shutdown at the height of the pandemic, and in those areas still battling pandemic surges.

- Cyber insurance rates, although currently stable, are expected to increase due to a raise in global ransomware claims.

- The last year has been one of the toughest years for the trade credit market. It’s estimated that trade credit insurers in the MENA area could face claims/loss ratios in excess of 100 percent in both 2020 and 2021.

- The business interruption and business protection insurance sectors have experienced exponential growth, as more and more companies look to protect their interests against future risks.

With the global and regional insurance markets in transition, it is more important than ever for insurers to provide coverage at affordable price points to ensure business continuity and protect cash flow while the global economy recovers.

The Road Ahead

Over the past year, the insurance industry witnessed many changes due to the global pandemic and subsequent economic consequences. The multi-pronged aspects of the pandemic impacted many lines of business where insurance coverage played a key role. The affected areas included, but were not limited to:

- Business interruption insurance (for example, disruption to supply chains and inability to operate as normal due to government measures)

- Trade credit insurance (cover for businesses if customers who owe money for products or services delay payment or do not pay at all)

- Travel insurance (to protect travel investments for business and pleasure)

- Cyber liability insurance (due to increased working from home)

- Event cancellation insurance (for both attendees and event hosts)

Insurers are facing a moment of truth. How they respond will lay a foundation for future resilience and growth. By preparing for the challenges of the future, they will be poised to face any changes with agility ensuring their clients are well protected in all facets of life.

Read More: