Medical Cover Demand to boost Takaful

Moody’s expects takaful premiums to grow moderately in the next two to three years, helped by rising demand for medical insurance within GCC, African and southeast Asian countries.

Takaful is set to see moderate growth with healthy prospects in the Gulf Cooperation Council (GCC) countries, Africa and southeast Asia, owing to a large Muslim population and fairly low insurance penetration. As more countries introduce mandatory health insurance, Moody’s Investor’s Service (Moody’s) expects the demand for Takaful products to increase, according to a new report.

The recent adoption of risk-based capital regulation in key takaful markets as well as takaful insurers’ momentum with respect to digitalisation, are further positive factors.

Low penetration

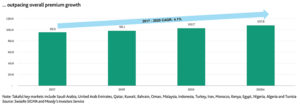

Takaful premiums/contributions grew at a healthy compound annual rate of 6.8 percent between 2017 and 2020, albeit down from 9.4 percent between 2011 and 2017, states the report. Overall, growth in takaful contributions has outpaced growth in total insurance premiums in the main takaful markets. Insurance penetration (gross written premiums as a percentage of GDP) in the takaful markets remains low, an indicator of good growth potential. The main takaful markets are (i) Malaysia and Indonesia in southeast Asia, (ii) the Gulf Cooperation Council (GCC) countries: Saudi Arabia, United Arab Emirates (UAE), Qatar, Kuwait, Oman and Bahrain, (iii) Turkey and Iran in the wider Middle East region, and (iv) Morocco, Kenya, Nigeria, Egypt, Algeria and Tunisia in Africa. In these markets, cumulative takaful premium growth has outpaced growth in overall insurance premiums, which expanded by 4.1 percent on average over the 2017 to 2020 period.

Compulsory cover

Takaful operators are well positioned to benefit from compulsory medical and motor cover, as they focus mainly on retail lines. Mandatory medical cover is also driving growth in southeast Asia and in Africa.

The introduction of compulsory medical insurance over the past few years in GCC counties such as Oman, Qatar, Saudi Arabia and Kuwait, and the implementation of mandatory motor insurance in Saudi Arabia in 2021, will help sustain takaful premium growth. The spread of mandatory health cover reflects government efforts to reduce public healthcare spending.

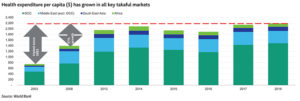

Total healthcare expenditure has grown considerably in all key takaful markets over the past two decades, partly reflecting higher demand for health insurance. Moody’s expects demand for private health insurance to grow further in response to the coronavirus pandemic. This will help offset reduced sales of group health cover as companies seek to cut costs amid slower economic growth.

Growing demand for health insurance, and a steady widening of mandatory medical cover, is also driving growth in takaful premiums in south east Asia and in Africa. For example, in Malaysia, health premiums grew 25 percentin 2019 as a result of the country’s National Health Protection Scheme. Egypt has also launched a phased introduction of compulsory health cover.

Growing demand for health insurance, and a steady widening of mandatory medical cover, is also driving growth in takaful premiums in south east Asia and in Africa. For example, in Malaysia, health premiums grew 25 percentin 2019 as a result of the country’s National Health Protection Scheme. Egypt has also launched a phased introduction of compulsory health cover.

Governments in key takaful markets are also encouraging consumers to build up their savings and make greater use of protection insurance. This will underpin growth in family takaful products, prompting insurers to acquire relevant licenses and expand their life insurance capabilities. Uptake of family takaful products is already strong in southeast Asia, and will increase more gradually in Africa and the GCC region.

Regulatory climate, digitalisation

It is expected that takaful operators’ capitalisation will remain strong as more governments introduce risk-based capital regulation, according to the report. Risk based capital regimes encourage better risk management, thereby improving insurers’ capital adequacy, underwriting, reserving and investments. Although these regulations are often not full economic capital regimes such as Solvency II, they nonetheless encourage better risk management. This improves insurers’ capital adequacy, underwriting, reserving and investments.

Better risk management will benefit the takaful industry over time, helping it overcome the challenges it currently faces. Takaful operators’ investment performance has come under pressure as a result of low interest rates and coronavirus-related market volatility. At the same time, intense competition, exacerbated by the pandemic-induced economic downturn, has weighed on insurers’ pricing power, undermining their profitability.

Other recent regulatory changes, such as a simpler licensing process for takaful operators in Kenya, Egypt, Morocco, Malaysia and Indonesia, are also positive.

The pandemic may delay payment of takaful insurers’ receivables (uncollected premiums). This will reduce their liquidity and trigger additional provisions, further weakening profitability and capital. This risk is more pronounced for insurers serving small and medium sized enterprises (SMEs) and corporate clients, as retail customers tend to pay premiums in cash upfront.

Takaful operators’ receivables also include some payments due from reinsurers. While these are mostly highly rated counterparties, they also include some non-investment grade and unrated names. In the GCC countries, there are also significant intermediary and inter-insurer balances that remain unreconciled and unsettled.

Takaful operators’ receivables also include some payments due from reinsurers. While these are mostly highly rated counterparties, they also include some non-investment grade and unrated names. In the GCC countries, there are also significant intermediary and inter-insurer balances that remain unreconciled and unsettled.

Takaful insurers will also benefit from consumers’ rapid switch to digital channels during the pandemic, which will allow them to reach more customers at lower cost.

Digitalisation, which allows insurers to reach more customers at lower cost, may help some takaful insurers achieve the necessary growth rates. The industry has been digitalising rapidly in response to the coronavirus pandemic, which has encouraged consumers to interact with their insurers mainly through online platforms. Customers have familiarised themselves with digital processes, and are now less likely to visit physical premises. Digital channels are also becoming the main distribution network for micro- insurance in Africa.

Takaful operators may also seek to grow through mergers and acquisitions. Takaful players in Saudi Arabia and Kuwait, where competition is making it harder for insurers to reach the critical mass required to meet new capital requirements, are particularly likely to pursue this option. Other recent regulatory changes, such as a simpler licensing process for takaful operators in Kenya, Egypt, Morocco, Malaysia and Indonesia, are also positive.