Bridging the GAP

Suresh Nair examines the relevance of GAP insurance in the GCC market.

Let’s start off with the story of Dom and Paul. Both are good friends and share a common love for cars and like taking out their cars for long drives. One day while out for a drive, navigating a sharp turn too fast the cars lost control and ended up crashing into each other. Initially they were furious with themselves. However they soon realised how lucky both of them were to escape with some minor scratches, though admittedly their egos were massively bruised. Both the cars were damaged very badly.

In the following weeks Dom following up with his motor insurers got a settlement offer. He promptly contacted the dealers from where he had bought his earlier (and now totalled) vehicle for buying a new car. To his shock, the quote given by the dealer for a similar specification of vehicle turned out to be almost double of the insurance settlement offer. This meant that Dom would need to fund the balance from his savings. He decided to give Paul a call to check how he was faring with his claim and was surprised to hear that Paul’s settlement was almost at the same as the price Paul would have to pay for the new car. Since both their cars, though different makes, were just under three years, Dom found the difference strange and queried Paul of the probable reason for this. Paul told him the main cause of the difference was the additional GAP insurance coverage he had taken. Dom was not familiar with GAP and asked for further details. Paul, who loved talking, elaborated as follows:

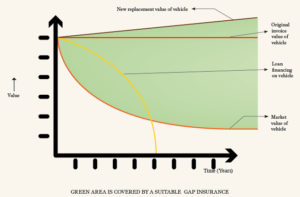

Guaranteed Asset Protection (GAP) is an insurance cover designed to to complement the normal motor comprehensive insurance. The value of a new car depreciates at a very high rate and this starts immediately when the car leaves the showroom. Depreciation rates, on a conservative basis, averages around 20percent annually though some vehicles depreciate much faster. Applying such a scale of depreciation, a car valued at AED100,000 when purchased will end up having a market value of AED50,000 or thereabouts after three years. In other words, a brand-new vehicle’s market value can go down to almost reach half of its original purchase price or thereabouts by the end of the first three years. The vehicle’s sum insured, if on a comprehensive basis, is linked directly to the market value which as stated earlier reduces continuously. This results in a sizeable gap opening between the original purchase price and the settlement value under the motor policy and this gap increases with each passing year. Hence in the event of the vehicle being declared a total loss or in the case of a theft occurring, the settlement which can be expected from the vehicle’s motor insurance will be lesser compared to the vehicle’s purchase value.

For vehicles bought with financing, the loan repayment is a factor of the loan amount (which is normally the vehicle value less any down payments) and the period of the loan. Anything happening to the car during the period of the loan can mean that there is an outstanding financial loan on the vehicle which still needs to be paid off. Very often for longer term loans the balance to be paid off can exceed the market value of the vehicle. The insurance pay-out is based on the market value, as alluded to earlier and does not cover the loan component. Hence after the accident it is quite possible that there is no longer a driveable vehicle in existence and the insurance pay-out is insufficient to even meet the requirements of closing the loan.

For vehicles bought with financing, the loan repayment is a factor of the loan amount (which is normally the vehicle value less any down payments) and the period of the loan. Anything happening to the car during the period of the loan can mean that there is an outstanding financial loan on the vehicle which still needs to be paid off. Very often for longer term loans the balance to be paid off can exceed the market value of the vehicle. The insurance pay-out is based on the market value, as alluded to earlier and does not cover the loan component. Hence after the accident it is quite possible that there is no longer a driveable vehicle in existence and the insurance pay-out is insufficient to even meet the requirements of closing the loan.

GAP policies are tailored for to meet these scenarios. The difference between the vehicle’s market value at the time of the accident/theft and the vehicle’s purchase price is bridged by the GAP policy. The policy, if so designed, can also cover outstanding loans on the vehicle. Hence with the right GAP policy, it is much more easier to get back on the roads with a new vehicle and no liability for outstanding payments to the bank or mortgage company.

Suresh Nair, executive director, Gargash Insurance

GAP insurance is bought as a supplementary cover to the normal motor comprehensive insurance and is most sold along with a new vehicle purchase. It is popularly sold by automobile dealers as a bundled offer along with the car, accessories, insurance, and other ancillary products. There is an option to purchase the GAP cover for periods longer than the usual 12 months. In certain cases where the coverage under the underlying motor comprehensive policy offers vehicle replacement, GAP coverage can be structured to kick in after this period to avoid duplication of cover.

“Are you still with me?” asked Paul to check if Dom was still tuned in. On hearing an affirmative grunt, Paul continued..

Several variants of the GAP product are available. The most common are”

Return to Invoice (RTI) – This type of GAP will pay the difference between the purchase price and the pay-out made under the comprehensive motor policy on the same vehicle in the event of a total loss or theft of the vehicle. Essentially the objective is to go back to the purchase price so that a replacement becomes possible.

Financial GAP insurance – In this case the difference between the outstanding loan on the vehicle and the pay-out under the motor policy as mentioned above will be paid under the GAP policy. This type of cover is linked to the financial loan. Clearly if a new vehicle is purchased with the customer making a down payment of 15-20 percent plus and financing the balance, GAP cover in the first year may not be of great use.

Replacement Vehicle Insurance (RVI) GAP – The payout here will equate to the difference between the new replacement cost and the motor policy payout which ensures that a replacement vehicle is available to the customer. The GAP claim is often settled by way of a credit voucher to the customer. This voucher is made in arrangement with the dealer who has sold the original car/GAP policy. This type of arrangement ensures a seamless transaction for the customer and translates into customer loyalty and retention for the dealer.

Claims under GAP in most cases would require proof of a total loss settlement made under the underlying motor policy and hence the exclusions attached to the latter policy would be applicable by default. These will include the usual general exclusions like causing the accident while driving under the influence of alcohol/drugs, driver not having a valid license at the time of the accident, wilful or gross negligence, sports trials, war, terrorism etc. Additionally, Gap does not pay any excess/deductible under the motor policy. In case of partial damages which are economically repairable, needless to add, the GAP cover will not operate.

In my case, Paul said, there always was the assurance that in the event of a serious car accident, any difference between the insurance settlement and the purchase price for the new vehicle would be picked up under the GAP insurance taken and I would be able to purchase a new car without needing to worry where the money was coming in from. Additionally, since the premium for the GAP insurance was rolled into the loan, I could pay it in parts. Dom nodded his head in understanding wishing that he had also bought out the GAP insurance for himself.

As we take leave of a now enlightened Dom, it is worthwhile looking at a few aspects which Paul did not talk about.

GAP is most commonly sold through the dealer though it can also be purchased from other sources. For the dealer, this provides a huge competitive advantage. For one thing it represents an additional touchpoint with the customer and an additional product to sell. More importantly GAP insurance works as a huge customer retention tool as it encourages customers to go back to the same dealer for a repeat purchase as explained above specially in context of RVI GAP. Overall, it is a great tool for customer retention and increasing loyalty.

GAP is most commonly sold through the dealer though it can also be purchased from other sources. For the dealer, this provides a huge competitive advantage. For one thing it represents an additional touchpoint with the customer and an additional product to sell. More importantly GAP insurance works as a huge customer retention tool as it encourages customers to go back to the same dealer for a repeat purchase as explained above specially in context of RVI GAP. Overall, it is a great tool for customer retention and increasing loyalty.

For the insurance industry, facing with a matured motor insurance market in most geographies, a new product line is always welcome. While some conventional motor policies provide an element of vehicle replacement these are generally restricted to new vehicles and for limited periods. Hence GAP provides a good additional product option specially as it bolts on quite well with the conventional motor policy with very similar sales talking points. It is noticed that while most insurers have motor insurance as part of their book, GAP insurance is only underwritten by a select number of companies. One possible reason could be the comparatively late development and entry of GAP as a product in the market. The other could be the nature of the product resulting in it being sold more through the dealer channel. Despite this there are compelling reasons for GAP like an available market, ease of design, reinsurance support, robust technology, and possibility of using available platforms for delivery of the product for Insurers to think seriously of making GAP a mainstream product.